The Risk-Based Approach:

What It Actually Means

Moving beyond compliance checklists to proportionate, evidence-based risk management

Most AML/CFT programs do not fail because they apply the wrong controls. They fail because they apply the same controls to everyone , and mistake uniformity for compliance. The risk-based approach is not a policy statement. It is a decision-making framework. Understanding the difference is the prerequisite for everything else.

What the Risk-Based Approach Actually Requires

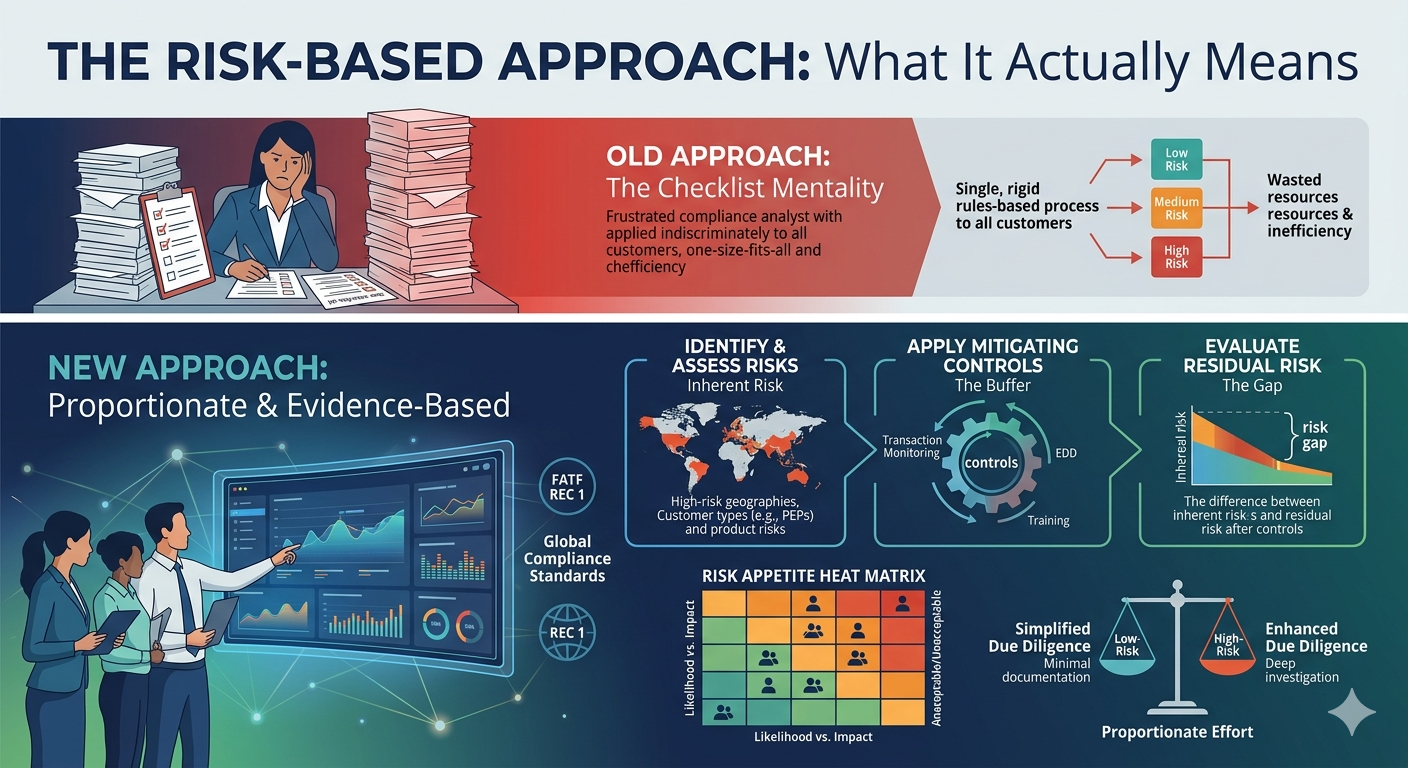

FATF Recommendation 1 places a clear obligation on financial institutions: identify, assess, and understand your money laundering and terrorist financing risks , and then apply measures that are proportionate to those risks. Four words that carry enormous operational weight.

Countries and financial institutions must identify, assess, and understand their ML/TF risks and apply AML/CFT measures proportionate to those risks , ensuring that higher-risk situations receive enhanced measures and that lower-risk situations may receive simplified measures.

, FATF Recommendations (2012, updated 2023); Immediate Outcome 1The critical implication , stated explicitly by the Wolfsberg Group , is that applying the same level of due diligence to all customers is not a risk-based approach. It is a rules-based approach. And a rules-based approach has a predictable, well-documented failure mode: it over-controls low-risk customers (consuming resource, degrading experience, inflating false positive rates) and under-controls high-risk ones (leaving material exposure undetected and unreported).

Applying the same level of due diligence to all customers is not an RBA , it is a rules-based approach that over-controls low-risk customers and under-controls high-risk ones.

The Three Consequences of Treating All Risk Equally

Cabinet Decision No. 10 of 2019, Articles 3–5, mandates adoption of an RBA calibrated to the type, size, and complexity of the financial institution. CBUAE AML/CFT Standards Section 4 requires documented risk assessments at product, channel, and customer levels , not a single institutional statement.

The Money Laundering Regulations 2017, Regulations 18–19, require Business-Wide Risk Assessments and Customer Risk Assessments proportionate to the nature and scale of the business. The FCA’s thematic reviews under its Financial Crime Guide (FCG 2.1) repeatedly cite failure to apply the RBA as a primary weakness, with enforcement action available under FSMA 2000, Section 206.

The Four COSO Risk Responses , and Their AML/CFT Equivalents

The COSO Enterprise Risk Management framework identifies four risk response options. In the context of AML/CFT, each maps to a distinct and consequential compliance decision. Understanding which response is appropriate , and being able to document why , is central to a defensible risk-based approach.

| COSO Response | Definition | AML/CFT Equivalent | Practical Example |

|---|---|---|---|

| Reduce | Apply controls to bring residual risk within appetite | Enhanced Due Diligence (EDD) | Senior management approval, source of wealth documentation, enhanced transaction monitoring frequency for a PEP relationship |

| Accept | Acknowledge the risk is within appetite; no additional controls | Standard CDD with documented rationale | A domestic retail customer with a low-value salary account , standard CDD is proportionate; no EDD required |

| Avoid | Exit or decline to eliminate exposure | De-risking / Relationship termination | Exiting a correspondent banking relationship where the counterparty fails a FATF mutual evaluation; declining onboarding of a customer from a sanctioned jurisdiction |

| Share | Transfer or distribute the risk | Product restriction / Contractual controls | Restricting remittance product features for certain corridors; imposing transaction limits as a condition of account opening in elevated-risk segments |

The COSO “avoid” response , translated in AML/CFT as de-risking , has attracted regulatory concern precisely because it is being applied as a default rather than a considered risk decision. Wholesale exit from entire customer segments or geographies, without evidence of individual risk assessment, is not an RBA. FATF and the Wolfsberg Group have both explicitly warned that indiscriminate de-risking is a failure of proportionality, not an application of it.

Making the Response Choice Defensible

A risk response is only defensible if it is preceded by a documented risk assessment. The response must be traceable back to a specific risk score, a specific risk category (ML, TF, or CPF), and a specific risk appetite threshold. Decisions made without this chain of evidence are vulnerable to regulatory challenge regardless of which response was chosen.

Inherent Risk, Residual Risk, and the Gap That Matters

The distinction between inherent risk and residual risk is not semantic. It is where most institutional risk reporting goes wrong , and where regulators look first when they want to understand whether a compliance program is genuinely effective or superficially compliant.

| Concept | Definition | Board Reporting Role |

|---|---|---|

| Inherent Risk | The risk exposure that exists before any controls are applied , a function of the institution’s products, customers, channels, and geographies | Sets the baseline. Without this number, the board cannot assess whether controls are proportionate to the actual risk level. |

| Control Effectiveness | The degree to which existing controls reduce inherent risk , assessed for design adequacy and operational performance | Explains the gap. If controls are poorly designed or inconsistently applied, they may not be reducing risk as assumed. |

| Residual Risk | The risk that remains after controls are applied , what the institution is actually exposed to | Must be compared to risk appetite. If residual risk exceeds appetite, remediation is required. |

Reporting only residual risk to the board conceals two dangerous gaps: (1) it prevents the board from assessing whether controls are proportionate to the actual risk level , they may be significantly under-resourced; (2) it prevents the board from detecting when controls are degrading, since residual risk can appear stable even as control quality deteriorates. Both inherent and residual positions must be reported, with the gap explained.

What the Inherent–Residual Gap Tells You

- A large gap with strong control evidence , suggests an effective, well-resourced control environment. The risk is being actively managed down.

- A small gap despite high inherent risk , is a red flag. Either the inherent risk is being underscored, or the controls are being over-credited. Both require scrutiny.

- A widening gap over time , may indicate controls are improving or inherent risk is declining. It may also mean the inherent risk scoring has been inflated to make controls appear more effective than they are.

- Residual risk that remains above appetite , requires a documented remediation plan with owner, timeline, and board sign-off. This position cannot simply be noted and moved on from.

When reviewing an EWRA, the most revealing test is to ask: what would the residual risk score be if the primary control failed completely? If the answer is “the same as inherent risk,” the control is working. If the answer is “we don’t know,” the control is not properly designed or its effectiveness has not been tested.

Risk Appetite: Beyond the Institutional Sentence

The most common failure in risk appetite documentation is also the most fundamental: treating risk appetite as a single sentence applicable to the whole institution. “We have zero tolerance for financial crime” is a mission statement. It is not a risk appetite statement , and it provides no operational guidance whatsoever to a compliance analyst making a real decision at an onboarding desk.

An institution’s risk appetite must be specific enough that a frontline staff member can use it to make a decision. If it cannot be applied to a specific customer, product, or transaction, it has not been defined , it has been declared.

Risk Appetite as a Product-Level and Segment-Level Statement

A functional risk appetite framework operates at the level where decisions are actually made: the product level and the customer segment level. Each combination requires an explicit appetite statement, a numerical threshold, and a defined consequence when that threshold is reached.

| Product / Segment | Risk Category | Appetite Threshold | Response Trigger |

|---|---|---|---|

| Trade Finance , Dual-Use Goods | CPF Risk | Residual score ≤ 12 (Medium) | Board Risk Committee review required if residual exceeds 12 |

| Correspondent Banking | ML / TF Risk | Inherent score ≤ 16 without Enhanced Controls | MLRO approval required; relationship restricted pending EDD |

| Virtual Asset Customers | ML / TF Risk | Residual score ≤ 15 (Medium-High) | Product suspension triggered above 15 pending control review |

| PEP Relationships | ML / Bribery Risk | Accept at residual ≤ 10 with full EDD pack | Senior management approval; 6-month EDD refresh mandatory |

| Retail , Low Value | ML Risk | Accept at standard CDD; residual ≤ 6 | Automated monitoring only; no enhanced review required |

The 5×5 Likelihood × Impact Scoring Matrix

Quantifying risk appetite requires a scoring methodology. The 5×5 likelihood × impact matrix is the most widely adopted approach across FATF-aligned institutions , and the approach explicitly supported by CBUAE Standards and the Wolfsberg FAQ methodology.

| IMPACT → | ||||||

|---|---|---|---|---|---|---|

| 1 Minimal | 2 Minor | 3 Moderate | 4 Major | 5 Severe | ||

| LIKELIHOOD ↑ | 5 Almost Certain | 5 | 10 | 15 | 20 | 25 |

| 4 Likely | 4 | 8 | 12 | 16 | 20 | |

| 3 Possible | 3 | 6 | 9 | 12 | 15 | |

| 2 Unlikely | 2 | 4 | 6 | 8 | 10 | |

| 1 Rare | 1 | 2 | 3 | 4 | 5 | |

The UAE National Risk Assessment (2020) identifies real estate, virtual assets, trade finance, and cash-intensive businesses as elevated-risk categories. Under CBUAE Standards, institutions operating in these sectors must ensure their likelihood scores in the 5×5 matrix reflect the NRA findings , an inherent likelihood score of 1 or 2 for a UAE-based virtual asset business is unlikely to survive regulatory scrutiny.

The Five Most Common RBA Failure Patterns

The FCA’s “Common and Emerging Financial Crime Risks” thematic reviews, FATF mutual evaluation findings, and CBUAE inspection reports converge on the same failure patterns with remarkable consistency. None of them require sophisticated analysis to identify. They are structural, systematic, and avoidable.

The Narrative EWRA

The Enterprise-Wide Risk Assessment exists as a descriptive document , lengthy, well-formatted, and entirely without numerical scores. Risk is described qualitatively (“elevated”, “significant”) with no scoring methodology. There is no way to prioritise, compare, or track risk over time. Regulators cannot assess proportionality without numbers.

ML, TF, and CPF Conflated

A single “financial crime risk” score is applied to all three categories. ML, TF (terrorist financing), and CPF (proliferation financing) have different typologies, different regulatory obligations, different control sets, and different national risk assessment conclusions. Treating them as one category means controls are designed for none of them specifically.

The Annual Calendar Trap

The EWRA is updated once per year on a fixed schedule regardless of what happens in between. FATF grey-listings, new sanctions regimes, product launches, significant volume changes, and enforcement actions against peers do not trigger a reassessment. The institution’s documented risk position can be materially wrong for months before anyone addresses it.

Institutional Appetite Statements

Risk appetite is documented as a single institutional statement , “zero tolerance for financial crime” or “low risk appetite for AML/CFT.” No product-level breakdown. No segment-level thresholds. No numerical triggers. Staff cannot use these statements to make decisions, and regulators cannot assess whether they are being applied.

Residual-Only Board Reporting

The board receives only residual risk positions. Inherent risk is absent from the report. The board cannot determine whether controls are adequately designed for the actual exposure level, cannot detect control degradation, and cannot make informed resource allocation decisions. The program may be passing inspection while failing structurally.

The FCA has taken enforcement action under FSMA 2000, Section 206 where failure to implement a genuine RBA was identified. Across FATF mutual evaluations, Immediate Outcome 1 specifically assesses whether the national and institutional RBA is well understood and effectively implemented , not merely documented. A well-structured EWRA document that does not demonstrably drive control decisions fails this test.

Jurisdiction-by-Jurisdiction: RBA Requirements

The RBA obligation is internationally consistent in principle but operationally specific in each jurisdiction. The following overview covers the four regulatory frameworks referenced in this article.

Mandates RBA calibrated to type, size, and complexity of the FI. Requires documented risk assessments at product, channel, and customer levels. The 2020 UAE NRA identifies real estate, virtual assets, trade finance, and cash-intensive businesses as elevated-risk categories that must directly inform RBA calibration. SCA Resolution No. 09 extends these requirements to securities firms.

Requires Business-Wide Risk Assessments and Customer Risk Assessments proportionate to the nature and scale of the business. FCA thematic reviews repeatedly cite failure to apply RBA as the primary weakness in financial crime programs. JMLSG Guidance Part I, Chapter 4 provides detailed risk factor guidance. Enforcement available under FSMA 2000, Section 206.

The foundational international RBA requirement. FIs must identify, assess, and understand ML/TF risks and apply proportionate measures. Sector-specific RBA frameworks exist for banking (2014) and virtual assets (2021). Mutual evaluations under Immediate Outcome 1 assess whether the RBA is both understood and operationally effective , not merely documented.

Operationalises the RBA into a structured risk assessment methodology covering four dimensions: customers, products, channels, and geographies. Explicitly states that uniform due diligence is a rules-based approach, not an RBA. Provides the practitioner-level methodology that sits between FATF principles and institutional implementation.

Building an Operationally Effective RBA: Six Steps

Regulatory alignment is the floor, not the ceiling. An RBA that does no more than satisfy the minimum documentary requirements is unlikely to detect the financial crime it is designed to prevent. The following steps translate principle into practice.

-

01

Separate ML, TF, and CPF as Distinct Risk Categories

Each has different typologies, different national risk assessment conclusions, and different control obligations. A single “financial crime risk score” cannot drive proportionate controls for all three. Your EWRA must have separate scoring tabs for each category, with independent inherent and residual positions.

-

02

Score Inherent Risk Using Actual Data , Not Assumption

Transaction volume breakdowns by product, customer demographic profiles, jurisdiction exposure maps, and product type analysis are the inputs , not narrative judgment. If your inherent risk scores cannot be traced back to a specific data source, they will not survive challenge.

-

03

Test Control Effectiveness , Not Control Existence

A policy is not a control. A form is not a control. An EDD checklist that is completed without genuine scrutiny is not a control. Control effectiveness testing requires sampling, testing operational performance, and measuring outcomes , not confirming that the procedure exists.

-

04

Set Numerical Risk Appetite at Product and Segment Level

Each product line and customer segment requires a documented appetite threshold on the 5×5 matrix. The threshold must be formally approved , board or board risk committee level , and must specify what happens when a risk score exceeds it: who is notified, what decision is required, and within what timeframe.

-

05

Maintain a Change Register for Between-Cycle Updates

Material events , FATF grey-listings, new sanctions designations, product launches, significant volume changes, peer enforcement actions , must trigger a targeted reassessment before the next scheduled EWRA cycle. The Change Register documents the event, the risk categories affected, the MLRO approval date, and the reassessment outcome.

-

06

Report Both Inherent and Residual Risk to the Board

Board reporting must show the inherent position, the residual position, the gap, and the control effectiveness assessment that explains the gap. Residual-only reporting prevents the board from performing its oversight function and will be identified as a governance failure in any serious regulatory examination.

Key Takeaways

- The RBA requires proportionate measures , not uniform procedures. Applying the same controls to every customer is explicitly not an RBA under FATF, Wolfsberg, UK, and UAE standards.

- The four COSO risk responses , reduce, accept, avoid, share , each map to specific AML/CFT decisions. De-risking is an “avoid” response and must be preceded by a documented individual risk assessment.

- Inherent risk must be reported to the board alongside residual risk. The gap between them is the single most revealing indicator of control effectiveness.

- Risk appetite must be set at product and segment level with numerical thresholds on a 5×5 matrix , not as a single institutional sentence.

- ML, TF, and CPF are separate risk categories requiring separate EWRA scores, separate controls, and separate board reporting lines.

- A Change Register is not optional. Material events between annual cycles must trigger targeted reassessments , not wait for the calendar.

Frequently Asked Questions

What is the difference between an RBA and a rules-based approach?

A rules-based approach applies the same controls to all customers regardless of their individual risk profile. An RBA calibrates controls to the assessed risk level of each customer, product, channel, and geography. The Wolfsberg Group states explicitly that uniform due diligence is not an RBA , it is a rules-based approach that simultaneously over-controls low-risk customers and under-controls high-risk ones.

Practically: a rules-based approach applies full EDD to every customer. An RBA applies standard CDD to low-risk retail customers, enhanced monitoring to medium-risk profiles, and full EDD with MLRO sign-off only to genuinely elevated-risk relationships , and documents the risk assessment that drives each decision.

Why must ML, TF, and CPF be assessed as separate risk categories?

The three categories have different typologies, different control obligations, different national risk assessment conclusions, and different regulatory reporting requirements. A customer posing elevated CPF risk (proliferation financing , sanctions evasion, dual-use goods) requires different controls to a customer posing elevated ML risk (structuring, layering through complex structures). A combined score cannot drive proportionate controls for either.

FATF has identified CPF as a distinct category since the 2012 Recommendations update, and CBUAE guidance explicitly requires separate assessment. Conflating the three is consistently identified as a primary weakness in UAE regulatory examinations.

How often should an EWRA be updated?

The EWRA should be formally reviewed on an annual cycle. However, material changes between cycles must trigger a targeted reassessment through a Change Register. Material events include: new product or service launches, entry into new geographies or customer segments, FATF grey-listing of a counterparty country, new sanctions designations affecting the portfolio, significant changes in transaction volumes, enforcement action against the institution or a peer institution, and significant changes in the compliance function including MLRO succession.

The MLRO should approve each targeted reassessment before normal business activity resumes in the affected area. An institution that updates its EWRA only on a fixed annual schedule , regardless of what happens in between , is not operating a genuine RBA.

What does “proportionate” mean in practice under FATF Recommendation 1?

Proportionality means that the intensity, frequency, and resource allocation of controls must match the assessed risk level. Higher-risk situations receive enhanced measures , more frequent review, more detailed documentation, senior management approval. Lower-risk situations may receive simplified measures , reduced verification requirements where national law permits.

Proportionality is assessed on the facts. An institution applying full EDD to routine low-risk retail customers is not being “cautious” , it is misallocating resources and signalling to regulators that no genuine risk differentiation is taking place. Both over-control of low-risk customers and under-control of high-risk ones represent failures of proportionality.

Is a 5×5 likelihood × impact matrix required, or are other scoring methodologies acceptable?

There is no regulatory mandate for a specific matrix format. FATF Recommendation 1 and its interpretive note require risk identification and assessment , not a particular scoring tool. The 5×5 matrix is the most widely adopted methodology because it is consistent with COSO ERM principles, produces a numerical score that can be tracked and reported, and is explicitly referenced in the Wolfsberg FAQ methodology.

What regulators do require is that the methodology is documented, consistently applied, produces comparable and trackable scores, and that the resulting scores demonstrably drive control decisions. A 3×3 or 4×4 matrix can satisfy these requirements if properly implemented. A purely qualitative assessment , “low”, “medium”, “high” without defined criteria , generally cannot.

How should risk appetite statements be presented to the board for approval?

Risk appetite statements should be presented as a structured schedule , one row per product line and customer segment , with the following columns: risk category (ML / TF / CPF), inherent risk score range, minimum control standard required, maximum acceptable residual score, and the consequence of exceeding that threshold (escalation path, approval required, product restriction trigger).

The board should formally approve the schedule, not merely note it. Minutes should reflect that the board challenged the appetite levels, understood the scoring methodology, and received assurance that the thresholds are being monitored. “The board noted the risk appetite statement” is not evidence of genuine board oversight.

From Principle to Practice

The risk-based approach is the conceptual foundation of every effective AML/CFT program , and the most consistently misapplied principle in the compliance landscape. Its requirements are neither new nor ambiguous. FATF has maintained the core obligation since 2003. What continues to fail is not understanding but execution: the gap between an institution that can describe the RBA and one that has genuinely built its compliance architecture around it.

The diagnostic test is simple. Take any compliance decision made in the past 30 days , an onboarding decision, a transaction monitoring alert disposition, a relationship review outcome , and trace it back to a documented risk score, a documented risk appetite threshold, and a documented control response. If that chain of evidence exists, the RBA is operating. If it does not, the institution may be compliant in appearance while remaining exposed in substance.

The remaining articles in this series build on these foundations: the EWRA as a live management instrument, program maturity diagnostics, and the quantitative tools that turn risk assessments into operational decisions. Each assumes that the reader has moved beyond treating the RBA as a regulatory obligation to be satisfied , and toward treating it as the analytical infrastructure that makes a compliance program genuinely effective.

Understanding Your EWRA: A Practitioner’s Guide , How to build, score, and maintain an Enterprise-Wide Risk Assessment that regulators respect. Covers ML/TF/CPF separation, data-driven scoring inputs, the Change Register, risk aggregation methodology, and the standalone Fraud Risk Assessment.