Understanding Your EWRA: A Practitioner’s Guide to Enterprise-Wide Risk Assessment

The Enterprise-Wide Risk Assessment (EWRA) is arguably the single most consequential document in a financial institution’s compliance architecture. It is the foundation upon which every downstream control from customer due diligence thresholds to transaction monitoring rule calibration — is built. Yet, in practice, too many EWRAs devolve into static annual exercises: a spreadsheet refreshed each December, rubber-stamped by the board, and filed away until the next regulatory examination. This guide is written for the practitioner who wants to move beyond checkbox compliance. We will dissect the structural, data-driven, and governance dimensions of the EWRA, drawing on requirements from the UAE, the UK, FATF standards, and Wolfsberg Group guidance to provide a framework that is both rigorous and operationally actionable.

◆

Separating ML, TF, and CPF: Three Distinct Risk Universes

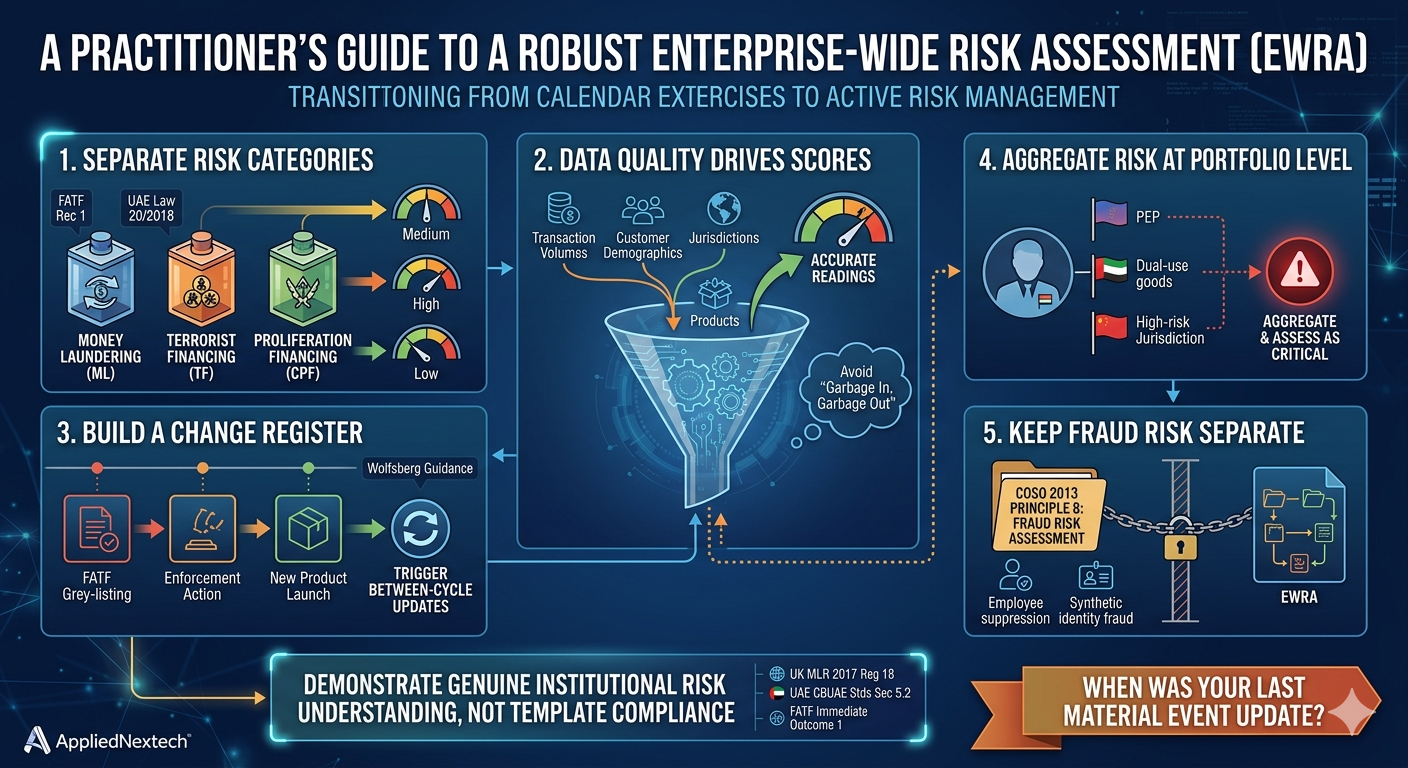

One of the most fundamental — and most frequently violated principles of EWRA construction is that money laundering (ML), terrorist financing (TF), and counter-proliferation financing (CPF) must be assessed as separate risk categories. These are not variations of the same threat; they involve different actors, different typologies, different red flags, and critically, different regulatory consequences. Conflating them produces a diluted assessment that fails to surface the unique control gaps each category demands.

Under UAE Federal Decree-Law No. 20 of 2018, Article 14(1)(a), and reinforced by Cabinet Decision No. 10 of 2019, Article 3, financial institutions are explicitly required to develop EWRAs that separately identify ML, TF, and CPF risks. The subsequent enactment of Federal Decree-Law No. 26 of 2021 elevated proliferation financing to a mandatory standalone risk category — not an appendix to the ML section. In the UK, MLR 2017, Regulation 18 requires documented Business-Wide Risk Assessments, while FATF Recommendation 1 and its Interpretive Note demand separate self-assessments for each risk type. FATF Recommendation 7 further mandates that PF risk be assessed and managed as a standalone category.

Merging ML and TF into a single risk score is a common examination finding. Regulators — particularly FATF mutual evaluation teams assessing Immediate Outcome 1 — treat this as evidence that the institution does not genuinely understand its risk exposure. Each category requires its own inherent risk score, distinct control mapping, and separate residual risk position with board-level visibility thresholds.

In practice, this means your EWRA should contain three parallel assessment tracks. TF risk, for example, must account for geographic nexus to conflict zones, customer links to designated entities, and the typically low-value, high-frequency pattern of terrorist financing transactions — none of which align neatly with ML indicators like structuring or layering. CPF risk requires analysis of dual-use goods exposure, trade finance corridors involving sanctioned jurisdictions, and end-user verification gaps — a fundamentally different control environment from either ML or TF.

◆

Data Inputs and the Quality Imperative

An EWRA is only as reliable as the data that feeds it. The scoring methodology — however elegant — collapses if the underlying inputs are incomplete, stale, or miscategorised. Four categories of data form the backbone of a credible EWRA:

Segment by product, channel, currency, and corridor. A bank processing $2 billion annually in correspondent banking flows through East African corridors has a materially different risk profile than one processing the same volume through intra-EU SEPA transfers.

PEP concentration, non-resident customer ratios, beneficial ownership complexity, and industry sector distribution. As the Wolfsberg Group’s PEP FAQ (2017, updated) emphasises, PEP concentration must be a specific EWRA data input — not an assumed constant.

Granular mapping of inbound and outbound flows by jurisdiction, cross-referenced against FATF grey/black lists, Transparency International CPI scores, and EU/UK high-risk third-country lists. UAEFIU Guidance Note No. 4/2021 prescribes this as an explicit EWRA content requirement.

Categorise products by inherent risk attributes: anonymity potential, cross-border capability, speed of settlement, and value transfer capacity. Private banking, trade finance, and virtual asset services each demand dedicated assessment.

Data quality failures are the silent killer of EWRA integrity. If your core banking system miscodes 12% of customer industry sectors, or your transaction monitoring platform cannot distinguish between wire transfers and internal book transfers, your EWRA inherent risk scores are mathematically wrong regardless of how sophisticated your scoring model appears. Validate data extraction queries independently before each EWRA cycle.

◆

The Change Register: Making the EWRA a Living Document

The most dangerous version of an EWRA is the one that was accurate — twelve months ago. Material events do not respect annual review calendars. A country added to the FATF grey list in March cannot wait until December to be reflected in your jurisdiction risk scoring. A new sanctions regime imposed overnight cannot remain invisible to your residual risk position for three quarters. This is where the Change Register becomes indispensable.

“Significant external events — FATF grey-listings, new sanctions designations, peer enforcement actions — must trigger between-cycle EWRA updates. The risk assessment is a living document, not an annual deliverable.”— Wolfsberg Group FAQ on Risk Assessments (2019)

The Change Register functions as a structured log of material events that have the potential to alter the institution’s risk profile. Each entry should capture: the event description, the date identified, the EWRA section(s) affected, the assessed impact (scoring change required or not), the action taken, and the date the EWRA was updated. The CBUAE AML/CFT Standards, Section 5.2, explicitly requires EWRA refresh after material changes not merely at the next scheduled review.

Examples of triggering events include: FATF grey-listing of a jurisdiction where the institution maintains significant correspondent relationships; enforcement actions against peer institutions for typologies present in your own product suite; launch of a new product with cross-border wire transfer capability; onboarding of a material new customer segment such as money service businesses; and changes to sanctions regimes affecting your trade finance corridors.

October 2022 — FATF Grey-Lists UAE

FIs with UAE exposure were required to immediately reassess jurisdiction risk scores and uplift correspondent banking due diligence. Institutions that waited for annual cycles faced supervisory criticism.

February 2023 — UAE Removed from Grey List

A second trigger event requiring EWRA update — removal from a grey list does not automatically reduce risk. Institutions had to evaluate whether underlying structural improvements justified score adjustments.

Ongoing — Peer Enforcement Watch

Major enforcement actions (e.g., FCA fines for trade finance controls failures) should prompt institutions offering similar products to re-examine their own control effectiveness scores in the EWRA.

Risk Aggregation: The Portfolio View and Compounding Factors

Individual risk factors rarely exist in isolation. A customer who is a Politically Exposed Person (PEP), deals in dual-use goods, and transacts through a high-risk jurisdiction presents a compounded risk profile that is qualitatively different from and far greater than the arithmetic sum of three medium-risk indicators. This is the principle of risk aggregation, and it is where many EWRAs systematically understate institutional exposure.

Your EWRA methodology must include explicit aggregation rules. Define which combinations of factors produce non-linear escalation. Document the thresholds at which compounded risk triggers board-level visibility. JMLSG Guidance Part I, Chapters 4.2–4.3, provides detailed content requirements that implicitly demand this portfolio-level synthesis, while UK MLR 2017, Regulation 18(4) requires proportionate documentation —meaning that the complexity of your aggregation methodology must match the complexity of your business.

Build a risk aggregation matrix that maps every plausible two-factor and three-factor combination against your risk rating scale. Test it with real customer profiles from your portfolio. If your highest-risk actual customer does not score at least “High” in the matrix, your methodology is miscalibrated. Present the matrix to the board alongside the top-25 highest-scoring customer profiles for validation.

◆

The Standalone Fraud Risk Assessment: Drawing the Boundary

A common structural error is embedding fraud risk within the EWRA. While fraud and financial crime share operational infrastructure (the same compliance team, often the same technology platforms), they are governed by different frameworks, involve different threat actors, and require different control architectures. COSO 2013 Principle 8 establishes that the fraud risk assessment must consider both internal and external fraud scenarios as a standalone exercise.

Internal fraud scenarios — employee threshold manipulation to avoid triggering alerts, alert suppression by complicit analysts, misuse of override authorities represent threats to the integrity of your AML controls themselves. They belong in a fraud risk assessment, not the EWRA, because they are about control subversion rather than customer-facing ML/TF risk.

External fraud scenarios — synthetic identity creation to bypass KYC, trade document falsification in letters of credit, and authorised push payment fraud intersect with AML typologies but operate through fundamentally different mechanisms. Synthetic identity fraud, for example, creates fictitious persons who pass CDD checks; the AML risk materialises downstream, but the root vulnerability is a fraud control failure.

If your fraud risk assessment is embedded as a chapter within the EWRA, examiners may conclude that neither assessment is fit for purpose. The EWRA is diluted by non-AML content, and the fraud assessment lacks the depth required by COSO Principle 8. Maintain separate documents with explicit cross-references where typologies overlap — for example, where trade-based money laundering intersects with trade document falsification.

◆

The EWRA is not a compliance deliverable — it is your institution’s risk intelligence platform. When constructed properly, it drives every material decision: how you allocate compliance resources, which products require enhanced controls, which customer segments warrant senior management attention, and where your residual risk sits relative to your board-approved risk appetite. Review your current EWRA against the five dimensions discussed here risk category separation, data quality, the Change Register, risk aggregation, and fraud assessment boundaries. Identify the gaps. Present them to your board with a remediation timeline. The institutions that treat the EWRA as a living, data-driven strategic document are the ones that withstand regulatory scrutiny and, more importantly, the ones that actually detect and prevent financial crime. Start your reassessment today.